The Ebola virus came as a shocker for everyone. No one was prepared for it. Many people lost their lives, and others lost their family members, jobs, and businesses. Most affected countries by this virus were Guinea, Sierra Leone, and Liberia.

The Ebola virus spread in Africa from 2014-2016. Africa is in its developing stage, so in 2014, when the Ebola virus was creating havoc out there, there was a lack of resources and healthcare. Until people came to know about the effects of this virus, a lot of destruction was already done.

Not only lives, but the economy in the affected countries also faced the hard consequences of this virus. But thanks to microfinance institutions, people were able to stand back on their feet. In this article, we are going to tell you about the role of microfinance institutions in post-Ebola recovery.

How Ebola Affected the Economy in Africa?

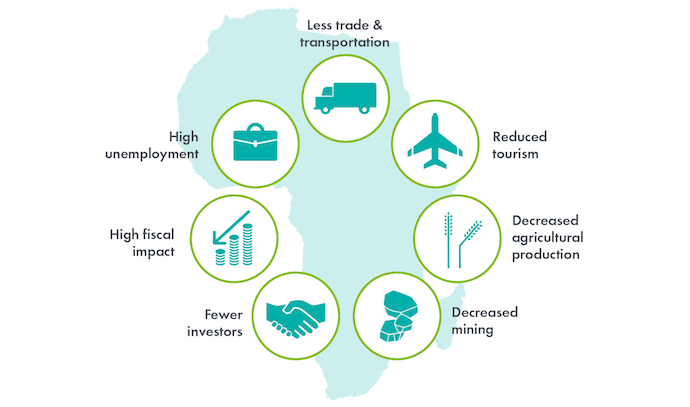

Just like other fields, the economy was also highly affected by the Ebola virus. The outbreak affected the economies of Guinea, Liberia, and Sierra Leone, the three countries that were hit the hardest. But interestingly, it is around the same time that Africa’s 2015 smartphone record-breaking sales happened. Coming back, here is how the economy was affected due to the Ebola virus.

1. Disruption of Trade and Business Activities

The outbreak resulted in the disruption of trade and business activities in the affected countries. Many businesses were forced to close, and cross-border trade was severely impacted. The traders were afraid to go to the affected parts of the country for any trade purposes. As a result, the economies of these countries suffered, and many people lost their jobs.

2. Decline in Agricultural Production

The Ebola outbreak also had a negative impact on agriculture, which is a critical sector in these countries. Many farmers were unable to tend to their crops or harvest their produce, leading to a decline in agricultural production. This directly affected the earning of the farmers.

3. Decrease in Foreign Investment

The Ebola outbreak caused a decrease in foreign investment in the affected countries. Many investors were reluctant to invest in these countries due to the health risks associated with the outbreak.

4. Increase in Government Spending

The governments of Guinea, Liberia, and Sierra Leone had to increase their spending to contain the outbreak. This included funding for medical supplies, healthcare workers, and other resources needed to combat the virus.

The increased government spending put a strain on these countries’ budgets and resulted in increased borrowing. However, since the government cannot always do everything, people must stay prepared for any future problems. For this, implications of how low-income households pay for healthcare in Mexico are a good example.

5. Decrease in Tourism

The Ebola outbreak also had a negative impact on the tourism industry in these countries. Many tourists canceled their trips, resulting in a decline in revenue for the tourism industry. All in all, the economy of majorly 3 countries including Guinea, Liberia, and Sierra Leone was harshly affected.

The Role of Microfinance Institutions in Post-Ebola Recovery

Even a small amount of money can be very helpful for someone in need. A good example of this is microfinance as a mobile game for teens. Microfinance institutions (MFIs) have played a very crucial role in post-Ebola recovery efforts by providing financial services to small and medium-sized enterprises and low-income households in affected communities. Here are some ways MFIs have contributed to the recovery efforts:

1. Providing Access to Money

Microfinance institutions provided access to capital for small businesses and households to help them rebuild and recover from the economic impact of the Ebola outbreak. This includes providing micro-loans, micro-insurance, and other financial services to help businesses get back on their feet.

2. Supporting Local Entrepreneurs

The institutions focused on supporting local entrepreneurs and SMEs that were most affected by the Ebola outbreak. By providing them with financial services and technical assistance, they helped these businesses to restart their operations and create employment opportunities in the affected communities.

3. Promoting Financial Inclusion

The Ebola outbreak highlighted the importance of financial inclusion in times of crisis. Microfinance institutions helped promote financial inclusion by providing financial services to previously underserved populations, including women, youth, and rural communities.

4. Strengthening Resilience

Microfinance institutions helped in building the resilience of affected communities and providing them with financial education and training. They educated people on financial management, budgeting, and savings strategies to help them better cope with future crises.

5. Collaborating with Other Stakeholders

The institutions worked in partnership with other stakeholders, including governments, non-governmental organizations, and development partners, to support the recovery efforts. This includes collaborating on financing programs, sharing best practices, and coordinating efforts to ensure that resources are effectively allocated to those in need.

Frequently Asked Questions (FAQs)

Q1. What did the government do to help Ebola?

The government took various steps to help Ebola and its spread. Here is the list of some of the steps taken by the government:

- Provided funding for medical supplies, healthcare workers, and other resources needed to combat the virus.

- Collaborated with other nations and asked for emergency funding to provide all the required resources to deal with Ebola.

- Encourages medical research to find cures for the Ebola disease.

- Increased the bedding facilities and other medical supplies in the hospitals.

- Made people aware of the virus and encouraged them to take all the necessary steps to prevent the spread of the virus.

However, just to be prepared for the future, an example can be taken from bundling mhealth info and microinsurance to improve health outcomes in Kenya.

Q2. What are the economic impacts of Ebola?

Just like other fields, the economy of Africa also faced a huge impact due to the Ebola virus. Here are some of the impacts of the Ebola virus on the economy.

- There was a huge decline in crop production which affected the earnings of farmers.

- Businesses that were mainly dependent on traveling, like tourism, transportation, etc, were affected because no one wanted to go to the infected areas.

- Foreign investors decreased their investment in Africa because of the Ebola virus.

Q3. What organization helped with Ebola?

There is not one but various organizations that helped in fighting the dangerous Ebola virus. Here is the list of some of those organizations.

- World Health Organization (WHO)

- Doctors Without Borders (Médecins Sans Frontières)

- Centers for Disease Control and Prevention (CDC)

- UNICEF

- International Medical Corps

- Samaritan’s Purse

- Red Cross

- The United Nations Mission for Ebola Emergency Response (UNMEER)

These organizations provided critical medical care, supplies, and support to those affected by the Ebola virus outbreak in West Africa, which began in 2014 and continued until 2016.

Conclusion

In summary, the Ebola virus outbreak had a significant impact on the economies of Guinea, Liberia, and Sierra Leone. The outbreak resulted in the disruption of trade and business activities, a decline in agricultural production, a decrease in foreign investment, an increase in government spending, and a decrease in tourism.

But the good part is, microfinance institutions took charge of the problem and provided loans to people who lost their jobs and businesses so that they could stand back on their feet and fulfill all their basic needs.

Author Profile

- Jonas Taylor is a financial expert and experienced writer with a focus on finance news, accounting software, and related topics. He has a talent for explaining complex financial concepts in an accessible way and has published high-quality content in various publications. He is dedicated to delivering valuable information to readers, staying up-to-date with financial news and trends, and sharing his expertise with others.

Latest entries

BlogOctober 30, 2023Exposing the Money Myth: Financing Real Estate Deals

BlogOctober 30, 2023Exposing the Money Myth: Financing Real Estate Deals BlogOctober 30, 2023Real Estate Success: Motivation

BlogOctober 30, 2023Real Estate Success: Motivation BlogOctober 28, 2023The Santa Claus Rally

BlogOctober 28, 2023The Santa Claus Rally BlogOctober 28, 2023Build Your Team – the Importance of Networking for Traders

BlogOctober 28, 2023Build Your Team – the Importance of Networking for Traders